We need your help!

How to contact your legislators: Enter your home address here to find their contact information. Or contact PDA's government relations team at (800) 223-0016 or djw@padental.org, and we'll provide you with the information you need.

What we’re asking for: Support for legislation that prohibits dental insurers from adopting a policy that they pay dental claims exclusively with virtual credit cards, requires insurers to notify dentists of other payment options, and gives dentists the ability to pick which one works for them.

Need a few talking points to help guide your discussion? See below. Thank you for being an advocate for your profession and patients!

Virtual Credit Card Talking Points (current 6/7/24):

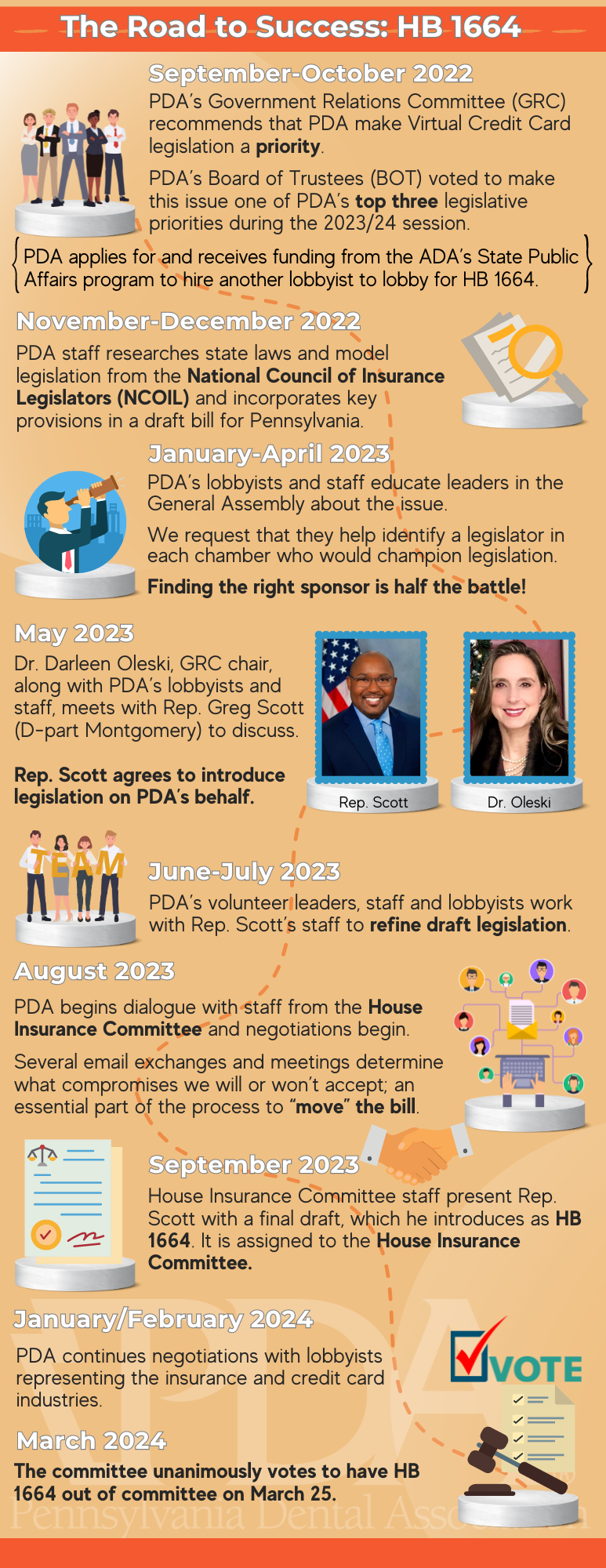

Follow the progress on the infograph and see more details about actions taken thus far in 2024. It’s critical for you contact your Senator by June 12th.